The latest report indicates that domestic smart sensor manufacturers are rising! MEMS is replacing traditional mechanical sensors!

Release time:

30 Aug,2022

Summary

I. Definition of Sensors

A sensor is a detection device that can sense the information of the measured quantity and convert the sensed information into an electrical signal or other required form of information output according to a certain law to meet the requirements of information transmission, processing, storage, display, recording, and control. It has the characteristics of miniaturization, digitization, intelligence, multi-functionality, systematization, and networking.

The upstream of sensors is various raw materials, including chips, circuits, power supplies, and different types of components; the midstream is various types of sensors, including capacitive pressure sensors, infrared gas sensors, and image sensors; the downstream is applied to consumer electronics, automotive electronics, industrial electronics, and communication electronics.

II. Sensor Industry Development Policies

In recent years, the state has provided a series of policy support for the sensor industry, promoting the improvement of the industry's technological level and the expansion of key application fields, and gradually achieving import substitution.

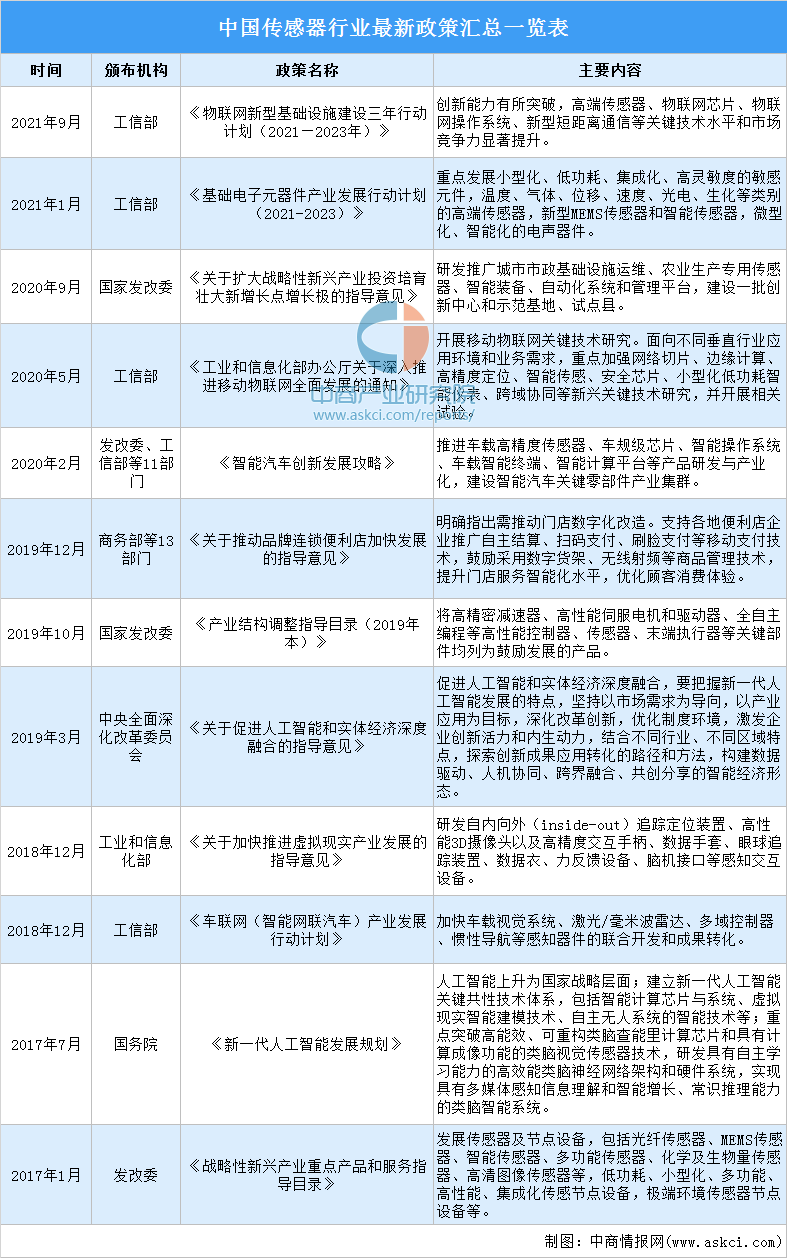

In January 2021, the Ministry of Industry and Information Technology issued the "Development Action Plan for the Basic Electronic Component Industry (2021-2023)", proposing to "focus on developing miniaturized, low-power, integrated, and high-sensitivity sensitive components, high-end sensors of temperature, gas, displacement, speed, photoelectric, and biochemical categories", bringing good development opportunities for domestic substitution of sensors.

III. Current Status of Sensor Industry Development

1. Sensor Market Size

Sensors are the bridge connecting the physical world and the digital world, referring to devices or instruments that can sense the specified measured quantity and convert it into a usable signal according to a certain law.

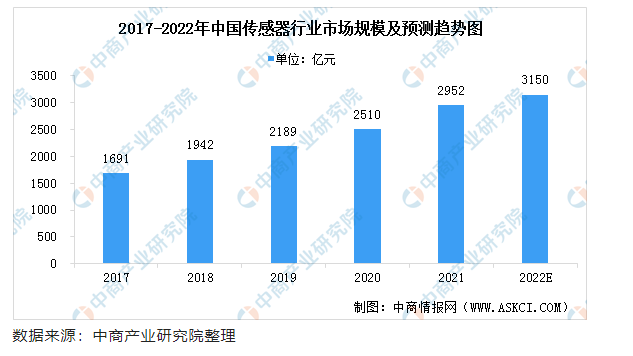

Data shows that in 2020, the size of China's sensor market was 251 billion yuan, a year-on-year increase of 14.7%. With the continuous progress of society, this industry has been increasingly valued under the empowerment of the Internet, and with the subsequent introduction of relevant supporting policies, the sensor industry market is promising. It is expected that the size of China's sensor market will further increase to 315 billion yuan in 2022.

2. Downstream Application Distribution of Sensors

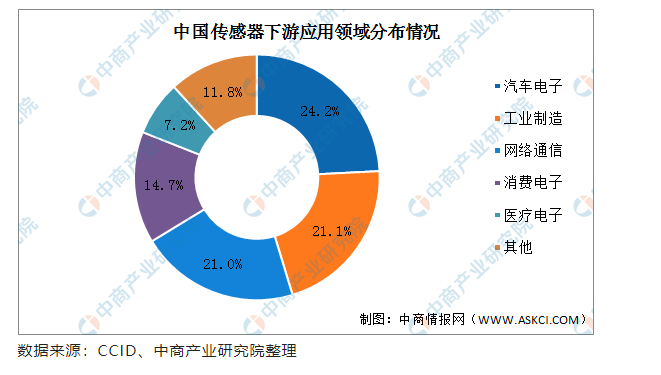

At present, China's sensors are widely used in automotive electronics, industrial manufacturing, network communication, consumer electronics, and medical electronics.

Data shows that Sensors account for the highest proportion in the automotive electronics field, reaching 24.2%; secondly, the proportion of sensors in the industrial manufacturing field is 21.1%, ranking second; the proportion of sensors in network communication, consumer electronics, and medical electronics fields are 21%, 14.7%, and 7.2%, respectively.

3. Market Size of Smart Sensors

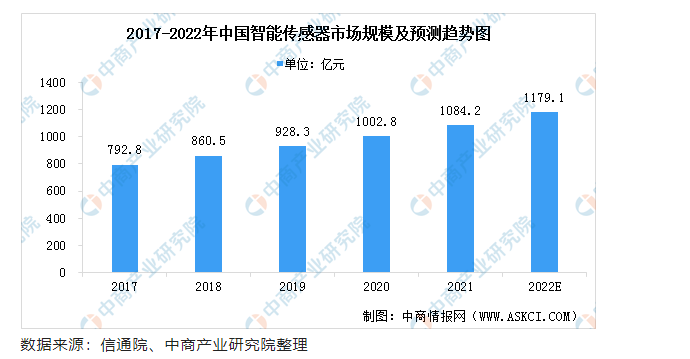

The steady growth of the sensor market has laid the foundation for the development of smart sensors. The size of China's smart sensor market has increased from 79.28 billion yuan in 2017 to 92.83 billion yuan in 2019. During the same period, the output value of smart sensors from domestic manufacturers increased from 9.49 billion yuan to 25.07 billion yuan, with the growth rate of domestic production significantly higher than the overall market growth rate. It is expected that by 2022, the market size of China's smart sensor industry will reach 117.91 billion yuan.

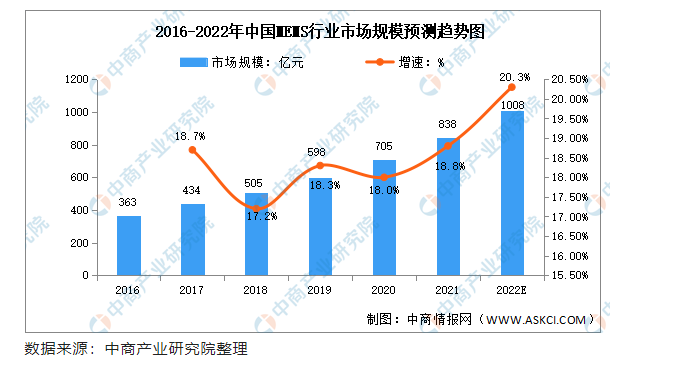

4. Market Size of MEMS Sensors

MEMS, or microelectromechanical systems, has competitive advantages such as miniaturization, low weight, low power consumption, low cost, and multiple functions compared to traditional mechanical systems. It can be mass-produced, packaged, and tested through micro-nano processing technology, so mass production and consistency are superior to traditional mechanical systems. 。

MEMS technology meets the needs of the consumer electronics market for small-size, high-performance sensors and is gradually replacing traditional mechanical sensors. Data shows that the market size of China's MEMS industry increased from 36.3 billion yuan in 2016 to 70.5 billion yuan in 2020, with a compound annual growth rate of 6.9%. Zhongshang Industry Research Institute predicts that the market size of China's MEMS industry will reach 100.8 billion yuan in 2022.

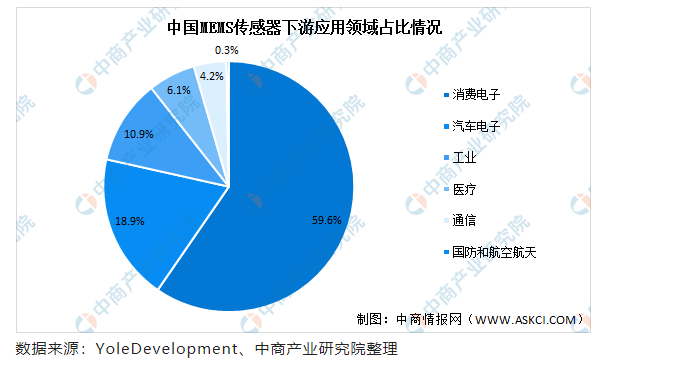

MEMS sensors, with their advantages of miniaturization, low cost, and multiple functions, are increasingly widely used in consumer electronics, automotive electronics, industry, medical care, and communication. In 2020, among downstream application fields, consumer electronics accounted for 59.6%, followed by automotive electronics at 18.9%, and industry at 10.9%.

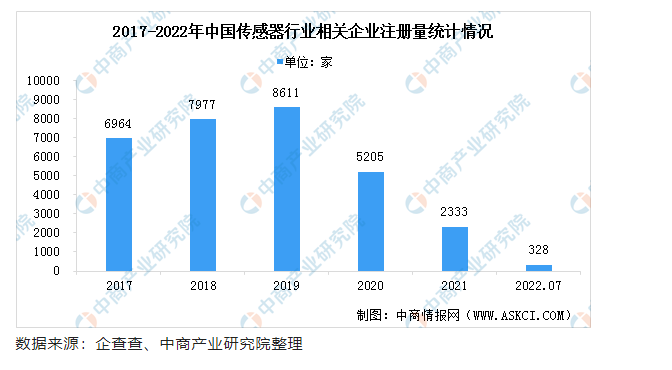

5. Registered Number of Sensor Industry Enterprises

Data from Qichacha shows that from 2017 to 2019, the number of registered enterprises related to sensors in China showed an upward trend, increasing from 6964 to 8611, with a compound annual growth rate of 11%. In 2020, affected by the COVID-19 epidemic, the number of registered enterprises related to sensors in China dropped to 5205, and further decreased to 2333 in 2021. As of July 2022, the number of registered companies related to the sensor industry is only 328.

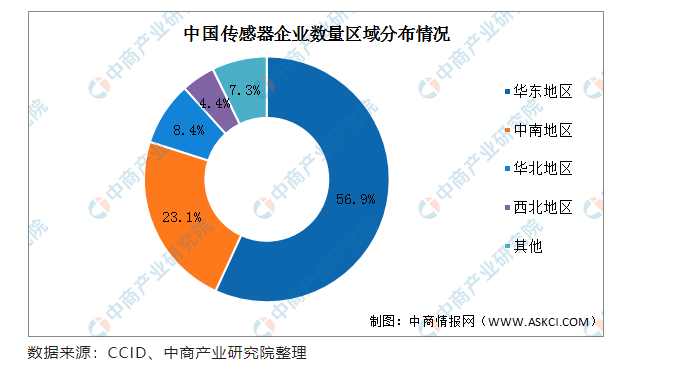

6. Regional Distribution of Sensor Enterprises

At present, the regional distribution of sensor enterprises in China is relatively concentrated, mainly in the East China region, accounting for more than 50%, about 56.9% of the total number of enterprises nationwide. Secondly, sensor enterprises in Central and South China account for 23.1% of the total number of sensor enterprises; the number of sensor enterprises in North China and Northwest China accounts for 8.4% and 4.4%, respectively.

7. Sensor Industry Market Competition Landscape

With the rapid development of China's informatization, China's sensor industry has developed rapidly in recent years. From the perspective of the competitive landscape, the top 5 sensor companies in China account for more than 40% of the domestic sensor market, and the industry's competitive landscape is gradually maturing.

Among them, HUT Sensor products are mainly used in smart travel, smart homes, smart healthcare, and smart cities. It is a globally influential sensor system solution provider with strong competitive advantages; Dali Technology is one of the few high-tech enterprises in China that can independently research and develop, and produce infrared thermal imaging related core chips, from core components to complete machine systems, with a complete industrial chain. Its sensor business accounts for over 90% of its total business, mainly producing infrared temperature imaging sensors. ; Goertek Currently, the revenue scale of precision components is relatively large. Goertek's sensors cover pressure sensors, interactive sensors, and fluid sensors, and are widely used in various consumer electronics products. It is in a leading position in the industry and has strong competitiveness.

V. Development Prospects of the Sensor Industry

1. Favorable Policies Promote Industry Development

The thermistor and sensor industry, as a basic and strategic industry of the national economy, plays an important role in promoting industrial transformation and upgrading and developing strategic emerging industries. At the same time, Affected by the international situation, the country attaches increasing importance to the development of the sensor industry, and its healthy development is in line with the national development strategy. In recent years, the state has provided a series of policy supports for the sensor industry, promoting the improvement of the industry's technological level and the expansion of key application fields, and gradually achieving import substitution.

In January 2021, the Ministry of Industry and Information Technology issued the "Development Action Plan for the Basic Electronic Component Industry (2021-2023)", proposing to "focus on developing miniaturized, low-power, integrated, and high-sensitivity sensitive components, high-end sensors of temperature, gas, displacement, speed, photoelectric, and biochemical categories", bringing good development opportunities for domestic substitution of sensors.

2. Downstream Application Expansion Drives Industry Development

More News

Tel: 400 006 6550

Office Address: 12F, Building I, International Innovation Park,

177 Songling Road, Laoshan District, Qingdao, Shandong, China